PADUCAH, Ky. (October 3, 2022) – Computer Services, Inc. (“CSI” or the “Company”) (OTCQX: CSVI) today reported its results for the second quarter and first six months of fiscal 2023, which ended on August 31, 2022.

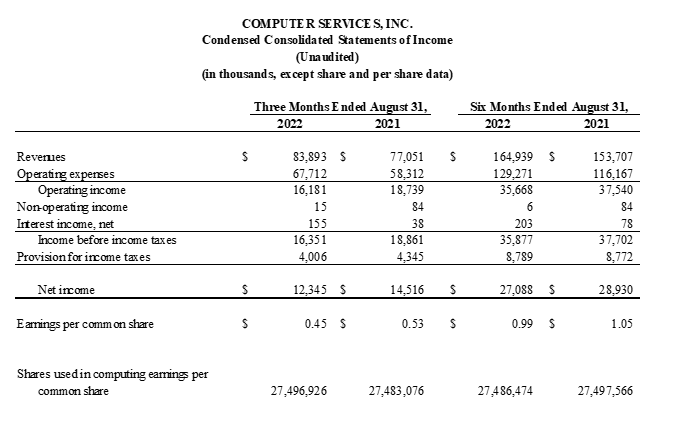

CSI’s revenues rose 8.9% to $83.9 million for the second quarter of fiscal 2023 compared with $77.1 million for the second quarter of fiscal 2022. Second quarter net income declined 15.0% to $12.3 million compared with $14.5 million for the second quarter of fiscal 2022. Net income per share was down 15.1% to $0.45 compared with $0.53 for the second quarter of fiscal 2022. The results for the second quarter included approximately $4.5 million in expenses related to financial and legal advisor fees related to the previously announced proposed acquisition of CSI by funds affiliated with Centerbridge Partners, L.P. and Bridgeport Partners (otherwise referred to herein as the “proposed acquisition”). Proforma adjusted net income, excluding the expenses related to the proposed acquisition and associated tax effect, was $15.7 million, or $0.57 per share, for CSI’s second quarter ended August 31, 2022 – See reconciliation of GAAP income to proforma adjusted net income included in the financial schedules of this release.

Second Quarter Results

Consolidated revenues increased 8.9% to $83.9 million in the second quarter of fiscal 2023 compared with $77.1 million in the second quarter of fiscal 2022. The growth in revenues benefited from higher sales in both the Enterprise Banking and Business Solutions groups, including growth in digital banking, payments processing, managed cybersecurity and document delivery revenues. The results for the second quarter of fiscal 2023 included $159,000 in early contract termination fees compared with $788,000 in the second quarter of fiscal 2022. Excluding the effect of early contract termination fees, net revenues increased 10.2% in the second quarter of fiscal 2023 compared with the second quarter of fiscal 2022. Early contract termination fees are generated when a customer terminates its contract prior to the end of the contracted term, a circumstance that typically arises when an existing CSI customer is acquired by another financial institution that is not a CSI customer. These fees can vary significantly from period to period based on the number and size of customers that are acquired and how early in the contract term a customer is acquired.

Operating expenses were up 16.1% to $67.7 million for the second quarter of fiscal 2023 compared with $58.3 million for the second quarter of fiscal 2022. The increase in operating expenses included approximately $4.5 million in expenses related to financial and legal advisor fees and other expenses related to the proposed acquisition. Excluding the $4.5 million in expenses related to the proposed acquisition, proforma adjusted operating expenses increased 8.5% to $63.2 million for the second quarter of fiscal 2023. The increase in proforma adjusted operating expenses for the second quarter of fiscal 2023 was primarily related to higher cost of goods sold on higher associated revenues and higher travel and software and hardware expenses.

Operating income declined 13.7% to $16.2 million for the second quarter of fiscal 2023 compared with $18.7 million for the second quarter of fiscal 2022. The decrease in operating income was due to the expenses related to the proposed acquisition. Excluding the expenses related to the proposed acquisition, operating income increased $1.9 million, or 10.2%, for the second quarter of fiscal 2023 compared with the second quarter of fiscal 2022. Operating margin was 19.3% in the second quarter of fiscal 2023 compared with 24.3% for the second quarter of fiscal 2022. Excluding the expenses related to the proposed acquisition, the proforma adjusted operating margin for the second quarter of fiscal 2023 was 24.6%.

The provision for income tax was $4.0 million for the second quarter of fiscal 2023 compared with $4.3 million in the second quarter of fiscal 2022. The decrease was due to lower taxable income in the second quarter of fiscal 2023 compared with the second quarter of fiscal 2022, net of a higher effective tax rate in the second quarter of fiscal 2023 compared with the second quarter of fiscal 2022.

Net income for the second quarter of fiscal 2023 declined 15.0% to $12.3 million compared with $14.5 million for the second quarter of fiscal 2022. Net income per share decreased 15.1% to $0.45 for the second quarter of fiscal 2023 on 27.5 million weighted average shares outstanding compared with $0.53 for the second quarter of fiscal 2022 on 27.5 million weighted average shares outstanding. Excluding approximately $4.5 million in expenses related to the proposed acquisition and $1.1 million of associated income tax effect, proforma adjusted net income for the second quarter of fiscal 2023 increased 8.3% to $15.7 million, or $0.57 per share.

Six Months Results

Consolidated revenues for the first six months of fiscal 2023 rose 7.3% to $164.9 million compared with $153.7 million for the first six months of fiscal 2022. CSI’s increase in revenues benefited from higher sales in both the Enterprise Banking and Business Solutions Groups, including growth in digital banking, payments processing, managed cybersecurity and document delivery revenues. Fiscal year-to-date revenues included $211,000 in early contract termination fees compared with $1.4 million in the first six months of fiscal 2022. Excluding the effect of the early contract termination fees from both periods, fiscal year-to-date revenues increased approximately 8.1% compared with the first half of fiscal 2022.

Operating expenses increased 11.3% to $129.3 million for the first six months of fiscal 2023 compared with $116.2 million for the first six months of fiscal 2022. The increase in operating expenses included approximately $4.8 million in expenses related to financial and legal advisor fees and other expenses for the proposed acquisition. Excluding the $4.8 million in expenses related to the proposed acquisition, proforma adjusted operating expenses increased 7.1% to $124.5 million for the first six months of fiscal 2023. The increase in proforma adjusted operating expenses for the first six months of fiscal 2023 was primarily related to higher cost of goods sold on higher associated revenues and higher travel and marketing from the in-person customer conference held in April 2022 and higher software and hardware expenses.

Operating income declined 5.0% to $35.7 million for the first six months of fiscal 2023 compared with $37.5 million for the first six months of fiscal 2022. The decrease in operating income was due to expenses related to the proposed acquisition. Excluding the expenses related to the proposed acquisition, operating income increased $2.9 million, or 7.8%, for the first six months of fiscal 2023 compared with the first six months of fiscal 2022. Operating margin decreased to 21.6% for the first six months of fiscal 2023 compared with 24.4% for the first six months of fiscal 2022. Excluding the expenses related to the proposed acquisition, proforma adjusted operating margin for the first six months of fiscal 2023 was 24.5%.

Net income for the first six months of fiscal 2023 declined by 6.4% to $27.1 million compared with $28.9 million in the first six months of fiscal 2022. Net income per share was down 5.7% to $0.99 per share for the first six months of fiscal 2023 compared with $1.05 for the first six months of fiscal 2022. Excluding approximately $4.8 million in acquisition related fees and $1.2 million of related income tax effect, the proforma adjusted net income for the first six months of fiscal 2023 increased 6.2% to $30.7 million, or $1.12 per share.

About Computer Services, Inc.

Computer Services, Inc. delivers core processing, digital banking, managed cybersecurity, information technology services, payments processing, document delivery, and regulatory and cybersecurity compliance solutions to financial institutions and corporate customers, both foreign and domestic. Management believes exceptional service, dynamic solutions and superior results are the foundation of CSI’s reputation and have resulted in the Company’s inclusion in such top industry-wide rankings as IDC Financial Insights FinTech 100, Talkin’ Cloud 100 and MSP 501 Top Global Managed Service Providers, for which it ranked second in 2021. CSI has also been recognized by Aite Group, a leading industry research firm, as providing the “best user experience” in its AIM Evaluation: The Leading Providers of U.S. Core Banking Systems. CSI’s stock is traded on OTCQX under the symbol CSVI. For more information, visit csiweb.com.

Non-GAAP Financial Measures

This release contains information prepared in conformity with GAAP as well as non-GAAP information. It is management’s intent to provide non-GAAP financial information to enhance an investor’s understanding of the Company’s consolidated financial information as prepared in accordance with GAAP. This non-GAAP information should be considered by the reader in addition to, but not instead of, the financial information prepared in accordance with GAAP. Each non-GAAP financial measure and the most directly comparable GAAP financial measure are presented so as not to imply that more emphasis should be placed on the non-GAAP measure. The non-GAAP financial information presented may be determined or calculated differently by other companies.

Additional information about non-GAAP financial measures, including, but not limited to, adjusted net revenue, pro forma adjusted net income and pro forma adjusted diluted EPS, and a reconciliation of those measures to the most directly comparable GAAP measures is included in the financial schedules of this release.

Forward-Looking Statements

This release contains “forward-looking statements” as that term is defined in the Private Securities Litigation Reform Act of 1995. All statements except historical statements contained herein constitute “forward-looking statements.” Forward-looking statements are inherently uncertain and are based only on current expectations and assumptions that are subject to future developments that may cause results to differ materially.

Readers should carefully consider: (i) economic, competitive, technological and governmental factors affecting CSI’s operations, customers, markets, services, products and prices; (ii) risk factors affecting the financial services information technology industry generally including, but not limited to, cybersecurity risks that may result in increased costs for us to protect against the risks, as well as liability or reputational damage to CSI in the event of a breach of our security; (iii) risk factors affecting the United States economy generally including without limitation acts of terrorism, military actions including war, and viral epidemics and pandemics that alter human behaviors, including the COVID-19 pandemic and its effect on our business operations and financial results; (iv) increasing domestic and international regulation imposing burdensome requirements regarding the privacy of consumer data especially consumer financial transaction data of which CSI possesses substantial quantities; (v) risks related to the proposed acquisition of CSI by Centerbridge Partners, L.P. and Bridgeport Partners; and (vi) other factors discussed in CSI’s Annual Reports, Quarterly Reports, news releases and other documents posted from time to time on the OTCQX website (www.otcmarkets.com), including without limitation, the description of the nature of CSI’s business and its management discussion and analysis of financial condition and results of operations for reported periods. Except as required by law or OTC Markets Group, Inc., CSI undertakes no obligation to update, and is not responsible for updating, the information contained or incorporated by reference in this report beyond the publication date, whether as a result of new information or future events, or to conform this document to actual results or changes in CSI’s expectations, or for changes made to this document by wire services or Internet services or otherwise.